On a recent trip home to Islay I picked up a copy of the Ileach (the local paper) and read an article relaying the pro-independence arguments that had been put forward by the Commonweal's Robin MacAlpine at a recent meeting there. Being familiar with the Commonweal's "White Paper Project", I felt compelled to respond.

***

I read with interest Chris Abell’s article in last month’s Ileach describing the Commonweal’s “strategy for winning independence”, as outlined by Robin McAlpine at a recent meeting on Islay.

Let me be clear about where I stand - there is after all no view from nowhere, there are merely different points of view. As Chairman of These Islands, a think tank which aims to encourage well-informed and civilised debate about the constitutional future of the UK, I have no party political allegiance but stand unabashedly for the view that more unites the nations of the United Kingdom than divides them (and I’m familiar with the Commonweal’s “White Paper Project”).

We’re told Mr MacAlpine is “unpersuaded by arguments that Scotland has neither the competence nor the resources for independence”. Unfortunately he is arguing against a straw man of his own making here, because nobody suggests that Scotland can’t be independent, we merely respectfully disagree about what the implications of such a move might be.

Claims that the Commonweal’s plans are “pragmatic and practical” and “do not dodge the difficult issues” deserve to be challenged.

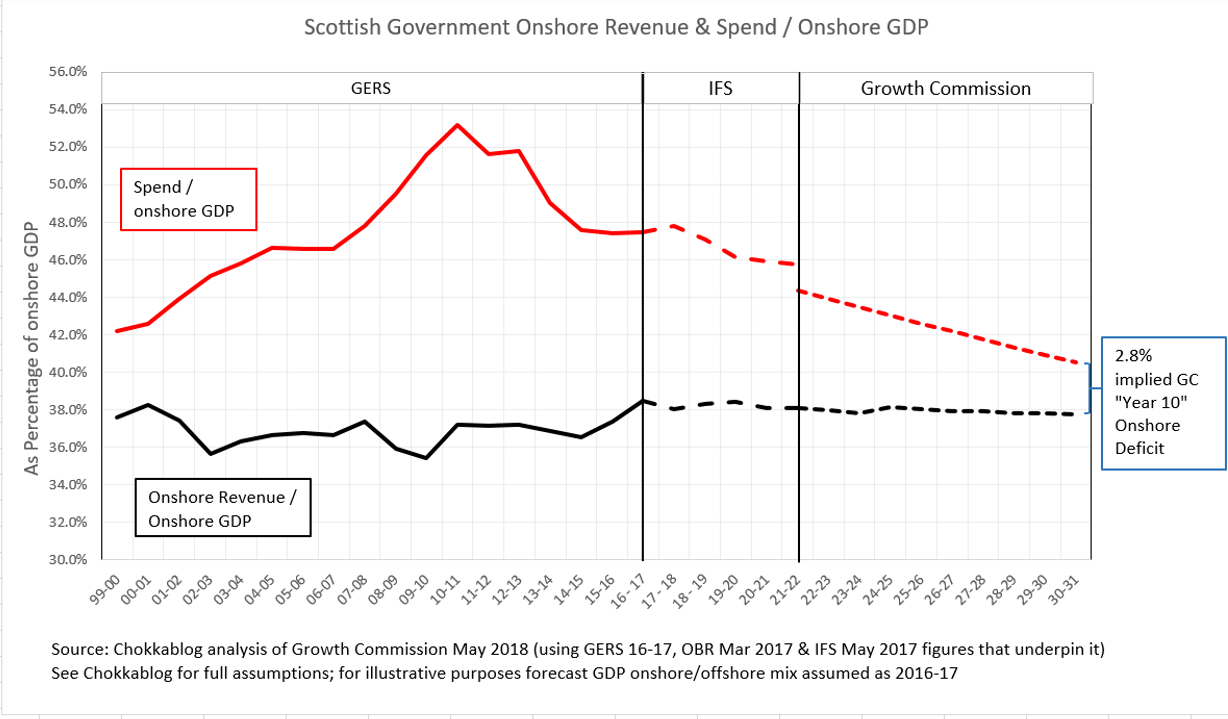

Scotland’s current deficit according to the Scottish Government’s own GERS figures is 7.9% of GDP. The Commonweal assume a Year One deficit for an independent Scotland of 5.5%, similar to the SNP’s own “Sustainable Growth Commission” assumption of 5.9%. These Islands has published a detailed paper (reviewed and endorsed by senior economists) which carefully explains why the assumptions used to reach these figures are not just heroically optimistic but in some cases fundamentally flawed.

Even if we accept these figures, a small independent country starting life with a deficit of more than 5.0% while trying to create its own currency would face huge challenges. For context: the EU’s “excessive deficit” threshold is set at 3.0% and the European Fiscal Compact specifies a 0.5% limit.

Contrast this with where we are today: the UK’s deficit is shared across our entire population, so the people of Scotland are currently only asked to bear their population share of a 1.9% deficit. So even to accept the Commonweal’s 5.5% figure is to accept that independence would make us materially poorer on day one. That difference of 3.6% of GDP is equivalent to over £6bn a year.

If we take the current GERS 7.9% figure as being a more realistic starting point, the figure becomes just over £10 billion or c.£1,900 a year for every man, woman and child in Scotland. That is the effective net fiscal transfer in Scotland’s favour as a result of the Barnett Formula, it is the tangible benefit of UK-wide pooling and sharing. Pointing out the fact that an independent Scotland would lose that transfer is not to suggest that Scotland couldn’t be independent, it is merely to highlight the very real implications for our capacity to invest in public services.

This simple fiscal arithmetic is why the SNP’s Growth Commission concluded that an independent Scotland would require at least a decade of further austerity. Nicola Sturgeon admitted as much in 2016 when challenged by Andrew Neil during a BBC interview: “we would deal with the deficit in the same way as the UK’s dealing with the deficit” she said.

So when pressed the SNP tacitly accept that independence would mean an extended period of further austerity. Given the additional challenge of being a new small country creating our own currency, it’s pretty clear that this would need to be far deeper austerity than anything we’ve experienced in recent times.

This context exposes the misleading nature of the Commonweal’s assertion that “nothing need change […] in health and social services, local government and policing”. A pragmatic and practical assessment that didn’t dodge the difficult issues would address the fact that significant cuts would be required to those public services which affect all of our day-to-day lives. The Commonweal’s paper simply fails to address this inconvenient truth.

After quoting research showing people “hate spinning, sarcasm and name calling and have little patience for negative campaigning and sloganeering”, MacAlpine apparently went on to talk of “the overwhelming shame of being governed from Westminster by a bickering crew of incompetent, lazy and lying politicians” and “their inability to look out for any interests but their own”. It’s a shame to read he resorted to such language, but it’s also unclear why he believes replacing politicians in Westminster (including 59 Scottish MPs) with more politicians in Holyrood would cure this problem – presumably it has something to do with our old friend Scottish exceptionalism?

There’s also an assertion that Brexit means independence is “beginning to make more sense to folk”. In fact for many of us the challenges of Brexit merely illustrate how much more destructive and painful breaking up the UK would be. Scotland is far more integrated with the UK than the UK is with the EU. As well as having full fiscal pooling and sharing (i.e. we share the deficit) we share a currency, defence and international affairs costs and have deeply integrated machinery of state. However bad Brexit may be, breaking up the UK would be an order of magnitude worse; two wrongs don’t make a right.

A final thought for those who suggest that Scotland receiving a fiscal transfer is evidence of economic failure under Westminster rule. The cause of Scotland’s higher deficit is mainly higher per capita spending rather than lower per capita revenue generation. Ileachs should understand this concept: just as Scotland is a relatively high “cost-to-serve” part of the UK, so Islay is of Scotland. Factor in the likes of Road Equivalent Tariff ferry subsidies, the costs of providing services to our remote communities and flights to the mainland for emergency medical procedures and I’m pretty sure Islay would have a higher per capita deficit than Scotland as a whole. The implied fiscal transfer that results is not evidence of an economic failing but of successful pooling and sharing, it demonstrates that we have a spirit of solidarity that goes beyond asking everybody to “pay their own way”.

Scotland benefits economically from being in the UK and the Scottish Government now has tax raising and benefits powers which would allow them to redistribute wealth very differently from today if they had the political will. Maybe the Commonweal should focus on how these hard-fought-for powers could be used to create a fairer Scotland in the UK rather than campaigning for a poorer Scotland outside it.

***

Wordcount discipline prevented me commenting on the hints about nationalising the Scottish whisky industry, the unfounded assertion that "support for independence has never been higher" or the fact that some of the ideas mentioned either are possible now with devolved powers or would fall foul of EU state-aid limits (the Commonweal is equivocal about future EU membership).

For completeness, this is the Ileach article I was respondong to: